Institute of Information Theory and Automation

You are here

Department of Econometrics

Deputy head:

Secretary:

Phone:

266052411

Fax:

266052232

Publications ÚTIA:

list Department of Econometrics focuses on understanding and modelling important economic and financial problems like decision making of agents, asset pricing, understating interaction between agents, or recently understanding the economic impacts of pandemics. We offer solutions to these problems with the help of mathematical models as well as statistical methodologies. More recently, we utilize modern machine learning methods for decision-making problems and analyze high-dimensional data sets (big data). We particularly focus on understanding economic and financial problems, focusing on estimation of real-world data.

In our department, we cover topics such as Machine Learning/Statistical Learning, Dynamic networks and financial decision making, Dynamic quantile asset pricing models, Measurement of dependence between cyclical economic variables, High-frequency data analysis, Agent based models, Stochastic optimization and Macroeconomics.

Working Papers:

- Moderation or indulgence? Effects of bank distribution restrictions during stress J. Barunik, J.A. Smith, E. Gerba and P. Katsoulis

Bank of England Staff Working Paper No. 1 053 (Nov 2023). - Common Firm-level Investor Fears: Evidence from Equity Options. J. Barunik, M. Bevilacqua and M. Ellington

preprint draft (Sept 2023) - Learning Probability Distributions of Day-Ahead Electricity Prices. J. Barunik, L. Hanus, preprint draft (Oct 2023)

- The Dynamic Persistence of Economic Shocks. J. Barunik, L. Vacha, preprint draft (June 2023)

- Currency Network Risk. M. Babiak, J. Barunik. preprint draft (May 2023).

- Dynamic industry uncertainty networks and the business cycle. J. Barunik, M. Bevilacqua and R. Faff. preprint draft (Mar 2021).

- Dynamic Network Risk J. Barunik, M. Ellington. submitted (2020).

- Deep Learning, Predictability, and Optimal Portfolio Returns. J Barunik, M. Babiak. preprint draft, Revise and resubmit, Journal of Banking and Finance (July 2021).

Selected Papers:

- Quantile Spectral Beta: A Tale of Tail Risks, Investment Horizons, and Asset Prices. J. Barunik, M.Nevrla, Journal of Financial Econometrics, 21(5), 2023, pp. 1590–1646.

- Moment set selection for the SMM using simple machine learning. E. Zila, J. Kukacka, Journal of Economic Behavior & Organization, 212(1), 2023, pp. 366-391.

- Estimation of heuristic switching in behavioral macroeconomic models. J. Kukacka, J.Sacht, Journal of Economic Dynamics & Control, 146, 2023. vol.146, 104585 [2023] Download DOI: 10.1016/j.jedc.2022.104585

- Persistence in Financial Connectedness and Systemic Risk J. Barunik, M.Ellington

European Journal of Operational Research, 2023, (forthcoming). - Asymmetric Network Connectedness of Fears. J. Barunik, M. Bevilacqua,

R. Tunaru. The Review of Economics and Statistics, 104(6), 2022, pp 1-13. - Do Rural Banks Matter That Much? Burgess and Pande (2005) Reconsidered. N. Buliskeria, J. Baxa, Journal of Applied Econometrics, 37(6), 2022, p. 1266-1274.

- Does parameterization affect the complexity of agent-based models? J. Kukacka, L. Krištoufek, Journal of Economic Behavior & Organization 192(1), 2021, pp. 324-356.

- Measurement of Common Risks in Tails: A Panel Quantile Regression Model for Financial Returns. J. Barunik, F. Cech. Journal of Financial Markets, 52, 2021.

- Multi-stage emissions management of a steel company. F. Zapletal, M. Šmíd, M. Kopa. Annals of Operations Research, 292, 2020, pp. 735–751.

- Forecasting dynamic return distributions based on ordered binary choice. S. Anatolyev, J. Barunik. International Journal of Forecasting , 35(3), 2019, pp. 823-835.

- Quantile coherency: A general measure for dependence between cyclical economic variables. J. Barunik, T. Kley. Econometrics Journal, 22(2), 2019, pp. 131-152.

- What type of finance matters for growth? Bayesian model averaging evidence. H. Iftekhar, R. Horvath, and J. Mares. The World Bank Economic Review, 32(2), 2018, pp. 383-409.

- Measuring the Frequency Dynamics of Financial Connectedness and Systemic Risk. J. Barunik, T. Krehlik. Journal of Financial Econometrics, 16(2), 2018, pp. 271-296.

- Do co-jumps impact correlations in currency markets? J. Barunik, L. Vacha. Journal of Financial Markets, 37(1), 2018, p. 97-119.

- Estimation of financial agent-based models with simulated maximum likelihood. J. Kukacka, J. Barunik. Journal of Economic Dynamics and Control, 85, 2017, pp. 21-45.

- Modeling and Forecasting Persistent Financial Durations. F. Zikes, J. Barunik, N. Shenai. Econometric Reviews, 36(10), pp. 1081-1110.

- Asymmetric volatility connectedness on the forex market. J. Barunik, E. Kočenda, L. Vacha. Journal of International Money and Finance, 77, 2017, pp. 39-56.

- Modeling and forecasting exchange rate volatility in time-frequency domain. J. Barunik, T. Krehlik, L. Vacha. European Journal of Operational Research, 251(1), 2016, pp. 329-340.

- Asymmetric connectedness on the U.S. stock market: Bad and good volatility spillovers. J. Barunik, E. Kočenda, L. Vacha. Journal of Financial Markets, 27, 2016, pp. 55–78.

- Semi-parametric Conditional Quantile Models for Financial Returns and Realized Volatility. F., Žikeš, J. Baruník. Journal of Financial Econometrics. 14 (1), 2016, pp. 185-226.

Organized conferences and workshops:

- STAT of ML 2023, 2022,2021,2020, 2019, Prague. Economterics Department in cooperation with Humboldt-Universität zu Berlin and Faculty of Mathematics and Physics, Charles University in Prague organized a STAT of ML (Statistics of Machine Learning) conference held October 5-6, 2023.

- Haindorf workshop 2022, 2020, 2019, 2018, 2017, 2016. The series of joint workshops with Humboldt University organized in January are focused on networking activities of research groups of prof. Barunik and prof.Hardle and training PhD students in statistical techniques. We have enjoyed hosting several respected scholars who joined the workshops including Victor Chernozhukov (MIT), Oliver Linton (Cambridge), Bryan Graham (UC Berkeley), Qiwei Yao (LSE), Holger Dette (Bochum) and many visiting international scholars.

- 2015 – 2020 Research Seminar Series – Jointly with Institute of Economic Studies we organize occasional small workshops for PhD students with invited international speakers, i.e. Eddie Gerba (LSE), Mattia Bevilaqua (LSE), Todorova (Bocconi).

- FinMaP – Financial Distortions & Macroeconomic Performance 2015 Prague: 2nd general workshop of the consortium organized by Institute of Information Theory and Automation.

- FinMaP – Financial Distortions & Macroeconomic Performance 2015 Mannheim: 3rd general workshop of the consortium co-organized by Institute of Information Theory and Automation.

- 2015 Econophysics Colloquium: The 2015 annual meeting of international researchers that brings together interdisciplinary research as physicists, economists and practitioners to discuss statistical methods, quantitative measures, modelling, simulations, and computational issues was co-organized in Prague by Institute of Information Theory and Automation and Charles University.

Department detail

Duration: 2020

- 2022

The project addresses the disconnection issue of the current financial and economic agent-based research. A complex agent-based economic model with an integrated financial sector will be suggested and a focus will be devoted to its econometric estimation. This interconnection will allow an overall study of the economic system under realistic assumptions about the behavior of economic agents.

Duration: 2020

- 2022

The project focuses on analysis of specific aspects of cryptoassets (cryptocurrencies), specifically on three main branches of research. First, we study the cryptoassets pricing mechanisms, mainly with respect to their fundamental factors such as number of users, number of transactions, traded volume, and others.

Duration: 2019

- 2023

The recent availability of large digital finance datasets brings new challenges to quantitative finance. Many of the classical financial econometric or optimization models become inappropriate or intractable when applied to digital finance data.

Duration: 2019

- 2021

The goal of this Project is to study arbitrage opportunities on limit order markets with boundedly rational agents.

Duration: 2018

- 2020

Multi-objective stochastic programming problems correspond to economic situations in which economic process is simultaneously influenced by a random environment and a decision parameter selected with respect to multi-objective optimization problem depending on the probability measure.

Duration: 2017

- 2019

The project focuses on utilization of multifractal framework in finance and financial economics. Specifically, we focus on three main branches of research. First, we examine how occurrence of financial extreme events translates into multifractal properties of the time series. For this purpose, we utilize the cusp catastrophe theory and the log-periodic power-law model.

- ‹ previous

- 2 of 8

- next ›

Fakulta sociálních věd UK

Fakulta sociálních věd UK

- ‹ previous

- 2 of 3

- next ›

2022-12-08

Jméno oceněného: František ČechOcenění: Soutěž o nejlepší publikaci ÚTIA pro rok 2022 - cena do 35 letOceněná činnost:...

2022-11-10

Jméno oceněného: L. Vácha, J. BaruníkOcenění: Nejlépe hodnocené kurzy na IESOceněná činnost: Výuka kurzu Advanced...

2022-10-30

Jméno oceněného: Jozef Barunik, Lenka NechvátalováOcenění: Zlatý kurz FSV Oceněná činnost: výukaOcenění udělil:...

2022-10-20

Jméno oceněného: Jozef Barunik, Lukas VachaOcenění: Zlatý kurz FSV (Financial Econometrics I)Oceněná...

2022-09-20

Jméno oceněného: Ladislav KristoufekOcenění: zařazení do Clarivate Highly Cited Researchers 2022 (10...

2021-11-30

Jméno oceněného: Jozef Barunik, Lenka NechvátalováOcenění: Zlatý kurz FSV (Applied Econometrics)Oceněná...

2021-11-20

Jméno oceněného: L. Vácha, J. BaruníkOcenění: Nejlépe hodnocené kurzy na IESOceněná činnost: Výuka kurzu Advanced...

2021-11-20

Jméno oceněného: L. Vácha, J. BaruníkOcenění: Nejlépe hodnocené kurzy na IESOceněná činnost: Výuka kurzu Advanced...

2020-11-30

Jméno oceněného: Evzen KocendaOcenění: GSJ Global Strategy Research PrizeOceněná činnost: For the best paper relating...

2020-11-20

Jméno oceněného: L. Vácha, J. BaruníkOcenění: Nejlépe hodnocené kurzy na IESOceněná činnost: Výuka kurzu Quantitative...

2020-11-10

Jméno oceněného: Jozef BarunikOcenění: Nejlepší magisterský kurs (Applied Econometrics)Oceněná činnost...

2020-10-10

Jméno oceněného: Martin Hronec Ocenění: Top 3 magistersky kurz Oceněná činnost: VyukaOcenění udělil: Institut...

Prof. Ing. Evžen Kočenda, M.A., Ph.D., DSc. received the scientific title "Research Professor in Social Sciences and...

Prof. Evžen Kočenda převzal 24.5. 2017 diplom s titulem „doktor sociálních a humanitních věd“ z rukou předsedkyne AV ČR...

Institute of Energy Economics, Faculty of Finance and Accounting, University of Economics in Prague awarded work of...

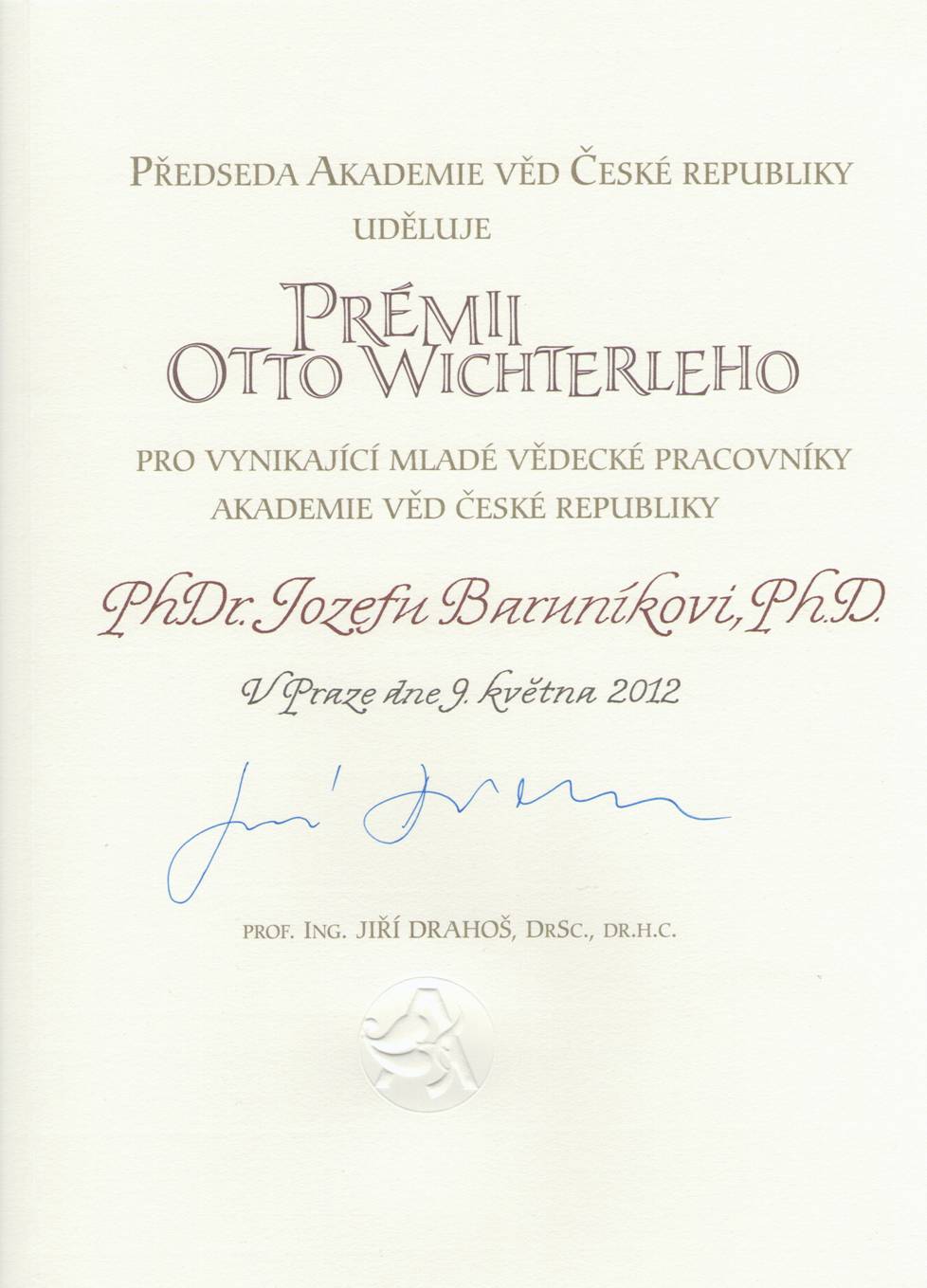

In the year 2014 the President of the Academy of Sciences of the CR granted The Otto Wichterle Award to promising young...

Česká národní banka udělila letošní cenu za nejlepší výzkumné práce (Economic Research Award) práci „Are Bayesian Fan...

The Czech National Bank has granted this year’s Economic Research Award to the paper “Are Bayesian Fan Charts Useful...

Institute of Energy Economics, Faculty of Finance and Accounting, University of Economics in Prague awarded work of...

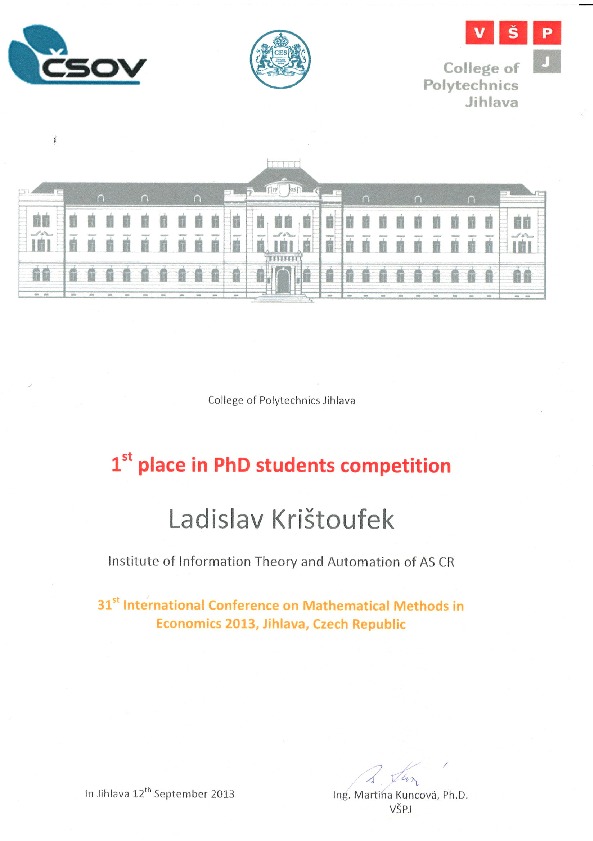

Ladislav Kristoufek was awarded by the 1st place in PhD students competition for his research paper "Mixed-correlated...

Institut energetické ekonomie při Fakultě financí a účetnictví VŠE ocenil práci Ladislava Krištoufka, Karla Jandy a...

In the year 2012 the President of the Academy of Sciences of the CR granted The Otto Wichterle Award to promising young...

2011-06-17

PhDr. Jozef Baruník získal první místo v 17. ročníku Souteže o nejlepší studentskou vědeckou práci z teoretické...